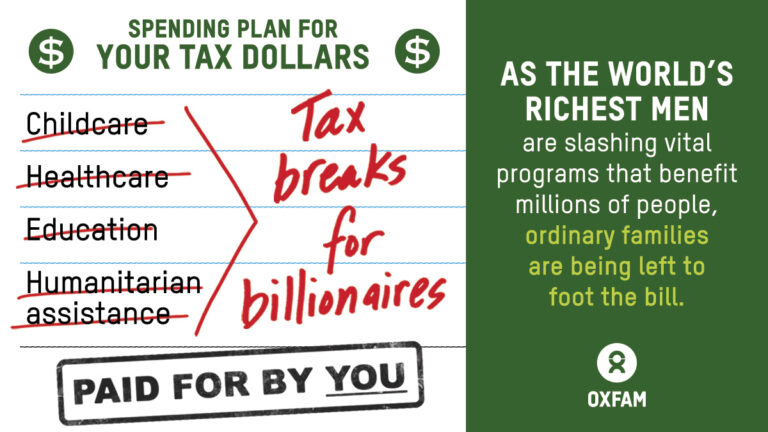

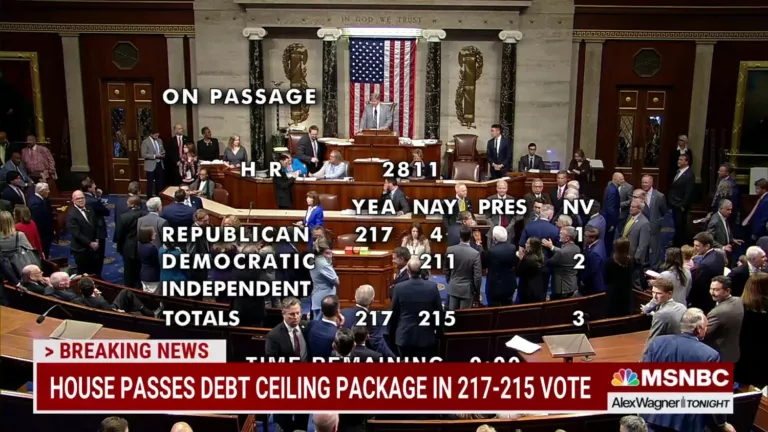

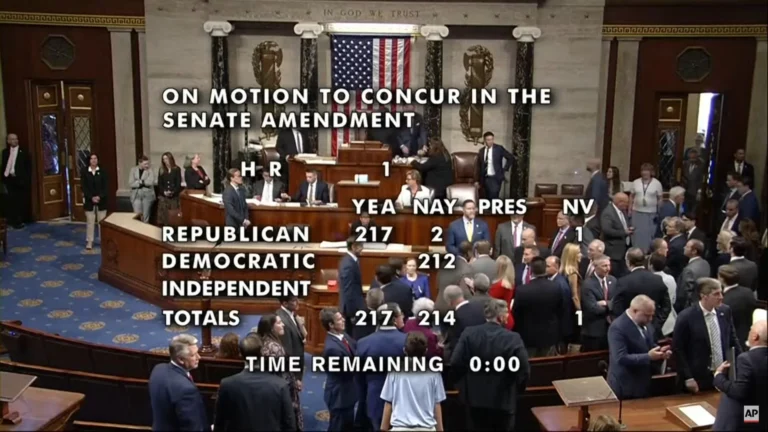

Arizona Democratic House Candidates React to the Passage of the Big Ugly MAGA Project 2025 Angel of Death Economic Bill

No surprises here. The Trump MAGA Know Nothing Republicans, having learned no history lessons from the economic poison unleashed by Trickle Down Economics in the Reagan, Bush II, and Trump I tax cuts, have, with no Democratic support, passed a Big Ugly MAGA Project 2025 Angel of Death Economic Bill that is supply side economics … Read more