Back in 2008, when predatory “payday lender” rules sunset under existing Arizona law, Jonathan “Payday” Paton convinced his fellow Tea-Publicans in the legislature to put Prop. 200 on the ballot, which would have extended existing exemptions for the payday loan industry regarding maximum interest rates.

Back in 2008, when predatory “payday lender” rules sunset under existing Arizona law, Jonathan “Payday” Paton convinced his fellow Tea-Publicans in the legislature to put Prop. 200 on the ballot, which would have extended existing exemptions for the payday loan industry regarding maximum interest rates.

The voters of Arizona resoundingly said “no” to the predatory practices of payday lenders.

But banksters never give up, and neither do their servile lickspitter servants in the lawless Tea-Publican Arizona legislature who badly want their campaign donations. The expressed will of the voters be damned — what do voters know anyway? Our authoritarian Tea-Publican legislators know what’s best for us. Just do as they say.

So once again, payday lenders are back with a bill to allow these predators to prey on Arizona citizens with HB 2611 (.pdf). The Arizona Capitol Times (subscription required) reported last week, Arizona House adopts bill to OK new loans for payday lenders:

The Arizona House passed a bill Wednesday that allows payday lenders to offer a new product with more than 200 percent interest, despite voters barring them from operating in the state under a 2008 initiative.

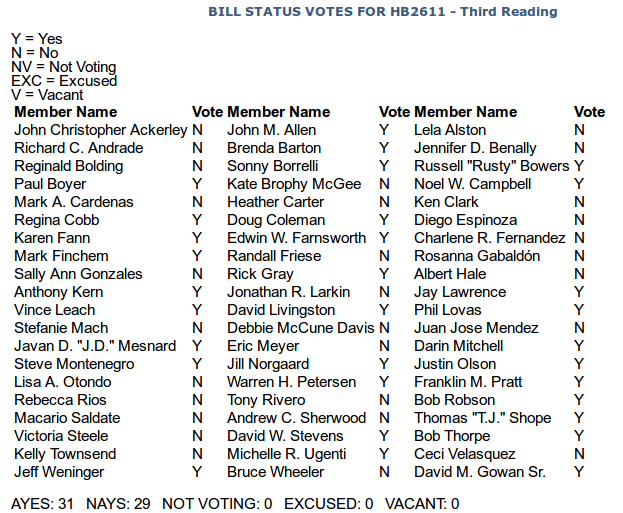

The proposal received approval in a 31-29 vote that included lawmakers from both sides of the aisle rising to champion their causes. [Vote detail at end of post.]

Bill sponsor J.D. Mesnard, R-Chandler, did not explain his vote but let fellow Republicans speak on the bill’s behalf.

Rep. Steve Montenegro, R-Litchfield Park, said “flex loan” companies provide a service for people with bad credit scores who have unexpected expenses. Montenegro said it’s unfair for Democrats to assume that residents will make decisions against their better judgment.

“Even if someone has a lower credit score that doesn’t also mean they have a lower IQ,” Montenegro said.

The old payday loans were issued after a borrower handed over a blank check that the lender agreed to hold for a couple of weeks — until the borrower’s next payday. They had interest rates and fees in excess of 400 percent a year.

The new loans are unsecured, but opponents note that lenders often require direct access to a person’s bank account so they can automatically deduct payments.

House Democrats said the bill would allow “predatory lending” to creep back into the state and prey upon Arizona residents.

Juan Mendez, D-Tempe, said the typically short duration of the loans virtually guarantees the need for repeat loans and creates a nearly inescapable cycle of debt.

“This isn’t a way to get back on your feet. This is economic slavery,” he said.

Rep. Reginald Bolding, D-Laveen, said although it may be important to provide lending options for people with bad credit, the bill allows loan companies to provide a product that will not benefit the consumer.

“We do want to provide options, but we don’t want to intentionally put bad options in the way of our constituents,” he said.

* * *

The legislation is being pushed by payday lenders through a group called the Arizona Financial Choice Organization. Many of the same players spent $15 million in the failed 2008 effort to get voters to allow them to continue to operate.

Former state Rep. Marian McClure (R-Green Valley), a very conservative lawmaker, is dismayed by HB 2611. She has penned two scathing op-ed opinions in the Green Valley News in recent weeks. In the first, IN MY VIEW: Flex Loans fees, rates will prey on the poor she writes:

It is dismaying to learn HB 2611 Flex Loans passed out of committee in the state Legislature.

This is a predatory lending scheme and should be defeated. The stated interest rate is 36 percent, however with the fee of a half percent per day based on the balance, the effective APR is 218.5 percent. The lenders will claim it is not interest but rather a fee. You may call a pig a sow but it is still a pig. Clearly, these loans will not benefit anyone other than the lenders.

* * *

According to a study in 2011, Payday loans took $1 billion out of the economy nationwide. If the flex loans are passed, I believe they will take millions out of the state economy because of the loss of buying power.

I spent six years battling the Payday loan problem until the people understood that 451 percent APR was not a good idea. With the people’s help, we were finally able to remove the blight of predatory payday loans.

I urge everyone to join me in calling, writing or emailing your state representative and senator and letting them know we in Arizona do not wish to have predatory lending and that you will be watching how they vote.

As you can see from above, the House did not listen to Ms. McClure. In her second op-ed she writes, EDITORIAL: Flex Loan advances, and the poor pay for it:

It is deeply disturbing to see 31 of my fellow Republicans vote in favor of financial rape of another human being. That is exactly what they did when they voted to allow HB 2611 Consumer Flex Loans to move out of the House of Representatives and go to the Senate.

In watching the vote and the explanations by the members, they kept referring to people that had sent letters in support. One Representative stated she had received such an email but after investigating she learned that the person worked for the Title Loan companies.

I would be willing to bet all the people that wrote those letters worked for the Title Loan companies or had loans with them.

They approved a daily fee of a half percent of the balance which is an APR of 182.50 percent plus the 36 percent interest rate. These loans may not exceed $3,000.

Let’s say that you take a loan for $3,000, the first month you will owe a fee of $450 plus $90 interest for a total of $540 before you even attempt to pay anything toward the $3,000 principle.

For many of us with good credit, this amount of fees and interest would seriously affect our budget and way of life. How much more so for those that are barely hanging on?

The argument is these are high risk loans and the lender is entitled to these fees. That was the same argument for payday loans. Since the payday lenders spent $14 million dollars fighting to stay in business in Arizona, I would say those loans were highly profitable.

If this bill should become law, it will be payday loans all over again. It will destroy families and do irrevocable harm to children.

* * *

One would have to seriously question the integrity or intelligence of anyone that supported this measure.

We have time to stop this erroneous bill in the Senate. Call 1-800-352-8404 and ask your senator to vote no on this bill.

Vote detail in the House.

Discover more from Blog for Arizona

Subscribe to get the latest posts sent to your email.

Always attacking the weakest link in our population. I thot this was resolved years ago. Shame on the legislator who revived tis scourge. VB

Perfect photo for this.

Any democrats vote yes? If so recall them also recall mesnard for trying thwart the will of the people even republicans will sign this recal petitions for being payday loan stooge.