Tea-Publicans like to claim that they are free market conservatives, let the “invisible hand” of the free market determine the winners and losers in the marketplace.

Only we have a real world example right now that this claim is total bullshit. Tea-Publicans are the servants to the Carbon Monopoly: oil, gas, and coal.

The first confrontation the new GOP Congress wants to pick with President Obama is over the Keystone XL Pipeline, at a time when the global price for sweet crude oil is in free-fall, dropping below $50 barrel today. Oil Price: Latest Price & Chart for Crude Oil – NASDAQ.com.

The first confrontation the new GOP Congress wants to pick with President Obama is over the Keystone XL Pipeline, at a time when the global price for sweet crude oil is in free-fall, dropping below $50 barrel today. Oil Price: Latest Price & Chart for Crude Oil – NASDAQ.com.

The “tight oil” from tar sands and shale oil are only profitable to extract and to refine when the price of oil is at $100 barrel or more. In short, the economics law of supply and demand is driving “tight oil” out of the marketplace (more on this below). So currently there is no market-based demand for the Keystone XL pipeline at the moment.

Charles Pierce at Esquire explains the GOP political motivation, Round One For The New Congress: The Keystone XL Pipeline:

The White House veto threat is not a categorical threat to the pipeline’s construction. The president is saying that the bill in question is premature, that it is short-cutting established procedure that already is underway, and that it is an improper federal infringement upon the function of the state judiciary of Nebraska. The president has not eliminated any of his options. While his most recent public statements indicate that he has soured considerably on the death-funnel, if his own State Department review were to approve the construction of the pipeline, the president would have considerable cover, and the death-funnel’s congressional fans would have a considerable weapon at their disposal.

But this skirmish today does nothing more than illustrate (again) that the Keystone XL pipeline has become little more than a fetish object for the political right. It needs to be built simply to anger the people who don’t want it to be built. It’s like watching people waving carved wooden totems at each other while chanting spells unintelligible to the uninitiated.

The fact is that the pipeline is inherently dangerous, that the fuel that it will carry is inherently poisonous, that the company seeking to build (and to profit by) the pipeline is inherently dishonest and that, until people in Nebraska started raising holy hell out on the prairie, the political process pushing the project was inherently fixed. None of these facts change no matter how devoutly you chant the spells. Those are the perils that the politicians who have lined up behind the death-funnel are willing to risk to hang a political scalp on the wall, the country’s breadbasket be damned.

In other words, more political posturing to pick a confrontation with the president to give the new GOP Congress a “win” to satisfy their conservative base at FAUX Nation, the actual economics of oil on the world market be damned.

On the economics of oil and the geopolitical consequences of the sudden collapse of the price of oil, Brad Plumer has a must-read analysis at Vox. com. Why oil prices keep falling — and throwing the world into turmoil:

The plummeting price of oil is still the biggest energy story in the world right now. It’s bringing back cheap gasoline to the United States while wreaking havoc on oil-producing countries like Russia and Venezuela.

* * *

The short version of the story goes like this: For much of the past decade, oil prices were high — bouncing around $100 per barrel since 2010 — because of soaring oil consumption in countries like China and conflicts in key oil nations like Iraq. Oil production couldn’t keep up with demand, so prices spiked.

But beneath the surface, many of those dynamics were rapidly shifting. High prices spurred companies in the US and Canada to start drilling for new, hard-to-extract crude in North Dakota’s shale formations and Alberta’s oil sands. At the same time, demand for oil in places like Europe, Asia, and the US began tapering off, thanks to weakening economies and new efficiency measures. On top of that, countries like Iraq began producing more oil.

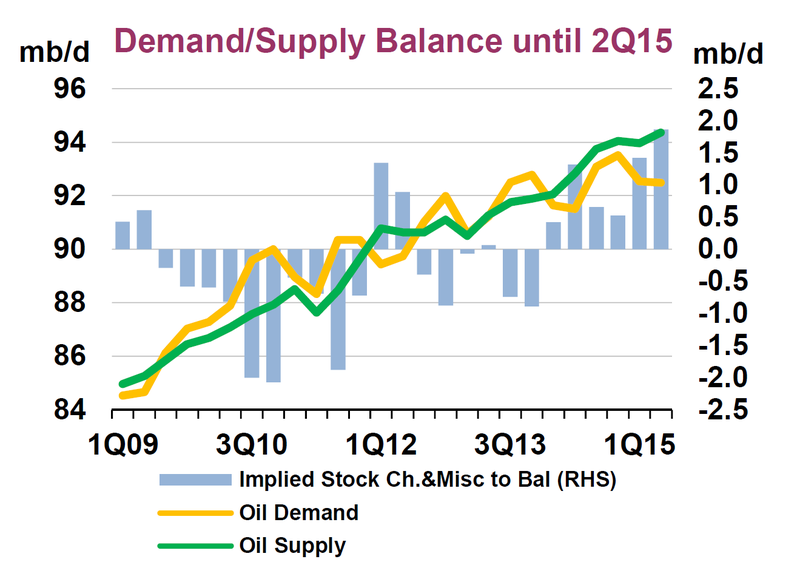

By late 2014, world oil supply was on track to rise much higher than actual demand, as the chart below from the International Energy Agency shows. And, in September, prices started falling sharply.

As prices slid, many observers waited to see whether OPEC, the world’s largest oil cartel, would cut back on its production to prop prices up.

As prices slid, many observers waited to see whether OPEC, the world’s largest oil cartel, would cut back on its production to prop prices up.

(Many OPEC states, like Saudi Arabia and Iran, need high prices to balance their budgets.) But at its big meeting in November, OPEC did nothing. Saudi Arabia didn’t want to give up market share, and it hoped that lower prices would help throttle the US oil boom. That was a surprise. So oil went into free-fall.

The oil price crash is now upending the global economy, with ramifications for every country in the world. Low prices are excellent news for oil consumers in places like Japan or the US, where gasoline is the cheapest it’s been in years. But it’s a different story for nations reliant on oil sales. Russia’s economy is facing a potential meltdown. Venezuela is facing serious unrest. Even better-prepared countries like Saudi Arabia could face heavy pressure if oil prices stay low.

* * *

Oil prices were rising sharply because global demand was surging — especially in China — and there simply wasn’t enough oil production to keep up. That led to large price spikes, and oil hovered around $100 per barrel between 2011 and 2014.

But as oil prices increased, many energy companies found it profitable to begin extracting oil from difficult-to-drill places. In the United States, companies began using techniques like fracking and horizontal drilling to extract oil from shale formations in North Dakota and Texas. In Canada, companies were heating Alberta’s gooey oil sands with steam to extract usable crude.

This led to a boom in “tight oil” production. The US alone has added 4 million new barrels of crude oil per day to the global market since 2008. (Global crude production is about 75 million barrels per day, so this is significant.)

Up until very recently, however, that US oil boom had surprisingly little effect on global prices. That’s because, at the exact same time, geopolitical conflicts were flaring up in key oil regions. There was a civil war in Libya. Iraq was a mess. The US and EU slapped oil sanctions on Iran and pinched its oil exports. Those conflicts took more than 3 million barrels per day off the market.

But much of this was changing by mid-2014. Many of those disruptions started easing. In July, Libyan rebels opened two key export terminals, Es Sider and Ras Lanuf, that had been shut down for a year. Libyan exports rose unexpectedly. (They have since fallen again as conflicts have flared up, but that’s been offset by rising production from Iraq, which is also getting its oil back online.)

Even more significantly, oil demand in Asia and Europe began weakening — particularly thanks to slowdowns in China and Germany. More broadly, oil demand has been stagnating in lots of places around the world. The United States, once the world’s biggest oil consumer, saw big cutbacks in industrial oil use after the recession, while gasoline consumption has flatlined as fuel-efficient cars became more widespread. At the same time, countries like Indonesia and Iran have been cutting back on fuel subsidies.

That combination of weaker demand and rising supply caused oil prices to start dropping from their June peak of $115 per barrel down to around $80 per barrel by mid-November.

* * *

At its big meeting in Vienna on November 27, there was a lot of heated debate among OPEC members about how best to respond to the drop in oil prices. Some countries, like Venezuela and Iran, wanted the cartel (mainly Saudi Arabia) to cut back on production in order to prop up the price. These countries need high prices in order to “break even” on their budgets and pay for all the government spending they’ve racked up.

On the other side of the debate was Saudi Arabia, the world’s second-largest crude oil producer, which was opposed to cutting production and willing to let prices keep dropping.

* * *

[T]he Saudis have signaled that they can live with lower prices in the short term. (The government has built up massive foreign-exchange reserves to finance deficits.)

In the end, OPEC couldn’t quite agree on a response and ended up keeping production unchanged. “We will produce 30 million barrels a day for the next 6 months, and we will watch to see how the market behaves,” said OPEC Secretary-General Abdalla El-Badri after the meeting.

That caused the price of oil to start crashing even further. The price of Brent crude went from $80 per barrel to $70 per barrel in just a few days. And it kept tumbling to down below $60 per barrel by mid-December.

For all intents and purposes, OPEC is now engaged in a “price war” with the US. What that means is that it’s relatively cheap to pump oil out of places like Saudi Arabia and Kuwait. But it’s more expensive to extract oil from shale formations in places like Texas and North Dakota. So as the price of oil keeps falling, some US producers may become unprofitable and go out of business. And the price of oil will stabilize. At least that’s what OPEC members hope.

The catch is that no one quite knows how low prices need to go to rein in the US oil boom. Analysts often focus on a metric called the “breakeven price” for oil-drilling projects.

* * *

If oil stays below $60 per barrel, some US companies will cancel or scale back shale drilling (a number of big companies are already pulling out of Texas’ Permian Basin for now). But other drillers may try to cut their costs, grit it out, and keep drilling. It really varies from company to company. That makes it very hard to predict how this all shakes out — or where global oil prices will bottom out.

Plumer continues with an analysis of Russia, Venezuela, Saudi Arabia and Iran, and how it affects the oil dependent economies of states in the United States.

This is a dangerous game that OPEC is playing. A global financial crisis and political revolutions in some countries could be the result of a prolonged oil price war. This is what we all should be concerned about.

But Tea-Publicans are instead paying off the Carbon Monopoly for its campaign donations, thus “picking winners and losers” in the supposedly “free market” economy, in which the economics law of supply and demand no longer supports “tight oil” from tar sands and shale oil. The GOP culture of corruption at its finest.

Discover more from Blog for Arizona

Subscribe to get the latest posts sent to your email.

Let me make sure I understand this. A Canadian company with a track record of dishonesty and shoddy maintenance practices turns pristine forest into a lunar landscape to get at the tar sands oil that lays beneath. Tar sands oil that is the nastiest stuff around. Cheapest way to get it to market is to send it cross-country to a Canadian port which is not going to happen as Canadians don’t want to take the leak/spill risk. So the Canadian company lobbies US politicians to route the stuff South through what Charles Pierce calls the most arable land in the nation, our breadbasket if you will, (where leaks/spills could permanently ruin that arable land (Dust Bowl scale catastrophe anyone?)) to a Gulf port where it’s marked for export to a foreign nation, probably China.

Upshot is many short sighted politicians are dying to allow a shady foreign company to potentially ruin our farmland for their profit and our loss. Not unlike the manner first world countries have treated the natural resources of third world countries for decades, if not centuries.

Judging from the speed the Republicans are trying to enact this, yeah, the fix is in.

I don’t think this a “payoff” to anyone. It is an example of thinking ahead. We may not need it right now, but we will need it in the future when the cost of a barrel of crude moves back to $100+.