Steve Benen has the November jobs report. Job growth remains strong, but short of last year’s pace:

Headed into this morning, the consensus forecasts pointed to job growth in November at about 261,000. We didn’t quite reach that total, but we got close.

The Bureau of Labor Statistics reported that the economy added 228,000 jobs in November, which is down slightly from October, but which is nevertheless a strong total reflecting a healthy market. The unemployment rate held steady at 4.1%, which is very low.

The revisions from the previous two months were mixed, with September’s totals revised up a little, but October’s totals revised down a little. Combined, they pointed to an addition 3,000 jobs added to the overall totals.

Providing some additional context, the U.S. added 1.97 million jobs over the first 11 months of 2012, 2.24 million over the first 11 months of 2013, 2.78 million over the first 11 months of 2014, 2.47 million over the first 11 months of 2015, 2.08 million over the first 11 months of 2016, and 1.91 million over the first 11 months of 2017.

Or put another way, while this year has been pretty good for job creation, we’re nevertheless on pace to see the slowest job growth since 2011.

Here’s another chart, this one showing monthly job losses/gains in just the private sector since the start of the Great Recession.

Economist Jared Bernstein adds, Jobs report: Another strong month as payrolls settle into solid trend, but wage growth still underwhelms:

The US labor market continues to add jobs at a strong clip, as robust consumer demand is generating a virtuous cycle of job growth, increased weekly hours, wage growth (though see ongoing caveats below), and hiring. Payrolls were up by 228,000 last month, above expectations for about 190,000. The unemployment rate held steady at 4.1 percent, a 17-year low.

Our official monthly jobs smoother filters out some of the noise in the payroll data by taking monthly averages over the last 3, 6, and 12 months. The fact that the bars are all about the same height reveals the underlying trend in job growth to be around 170,000 per month, a healthy pace for this stage of the recovery. As labor markets close in on full employment, job growth slows a bit as workers become more scarce.

However, given the movement of other key variables, namely, wages and prices, the full-employment, full-resource-utilization case cannot yet be made, as I show below.

Once again, hourly wage growth is a sore point. The two figures below show yearly wage growth for all private-sector workers and for the 80% of the workforce that’s blue-collar in goods production or non-managerial in services. In both cases, the 6-mos moving average reveal a flattening trend. Basically, in 2015-16, the tightening job market drove wage growth up from 2 to 2.5 percent, around where it has been stuck since. In fact, that’s precisely last month’s yearly growth rate for all private workers (2.5%). Given the consumer inflation has been running at around 2%, that’s but a small hourly wage gain in real terms, and certainly less than I’d expect given a 17-year low in the jobless rate.

That said, other series show stronger wage growth, as Dean Baker and I point out here, especially for middle-wage and minority workers, so the jury’s not in on the mystery of the missing wage growth. All told, in a series that mashes together 5 different wage series (which I’ll post later) we see a mild acceleration, but again, less than would be expected.

Also, hours worked per week ticked up last month and weekly earnings were up 3.1%, the strongest weekly growth rate since early 2011.

One theory is that the job market is pulling less skilled and experienced workers in from the sidelines, and this is holding down wage growth. But the Atlanta Fed tracker, which tries to control for this, doesn’t show much acceleration either.

All of this creates a challenging dynamic for the Federal Reserve. The next figure shows how the current unemployment rate of 4.1% is below the rate the Fed’s “natural rate,” i.e., the lowest jobless rate consistent with stable prices. But neither prices (core PCE, the Fed’s preferred gauge), which recently went through a bout of DEcelleration, nor wages, are responding much at all to low unemployment.

Are there, then, measures of labor demand that do not show a fully tight labor market? In fact, labor economists consider the employment-to-population ratio of prime-age (25-54) workers is a quick proxy for this question. This rate fell from about 80% before the last recession to 75% at its trough. It’s now at 79% so it has clawed back about three-quarters of its losses. In other words, it’s possible that the labor force still has some room-to-run and that labor demand, as strong as it is, still hasn’t exhausted labor supply.

* * *

Surely, some politician will say something foolish about how the solid November report reflects the tax cut that’s working its way through the Congress. [Cue or blog trolls.] If I could, I’d issue fines for such statements ($1.5 trillion sounds about right). As the smoother graph shows, we’re right on a trend that’s been ongoing for years now. As noted, there’s real momentum in the economy, with job gains, if not much in real hourly wage gains, boosting household incomes.

The challenge for policy makers, especially at the Fed, is to not get spooked by the strong quantity numbers (jobs) when the “price” measures–wages and inflation–are not flashing red at all.

Josh Bivens, the research director at the Economic Policy Institute adds, Wages really are rising too slowly. But corporate tax cuts won’t help.:

Republicans in Congress and the White House have clearly settled on a central theme to market recent plans to cut taxes on business: These cuts will end up boosting wages for American workers. As public relations, this theme is brilliant; too-sluggish growth in paychecks is a central concern for the American public. As economics, however, it’s bunk.

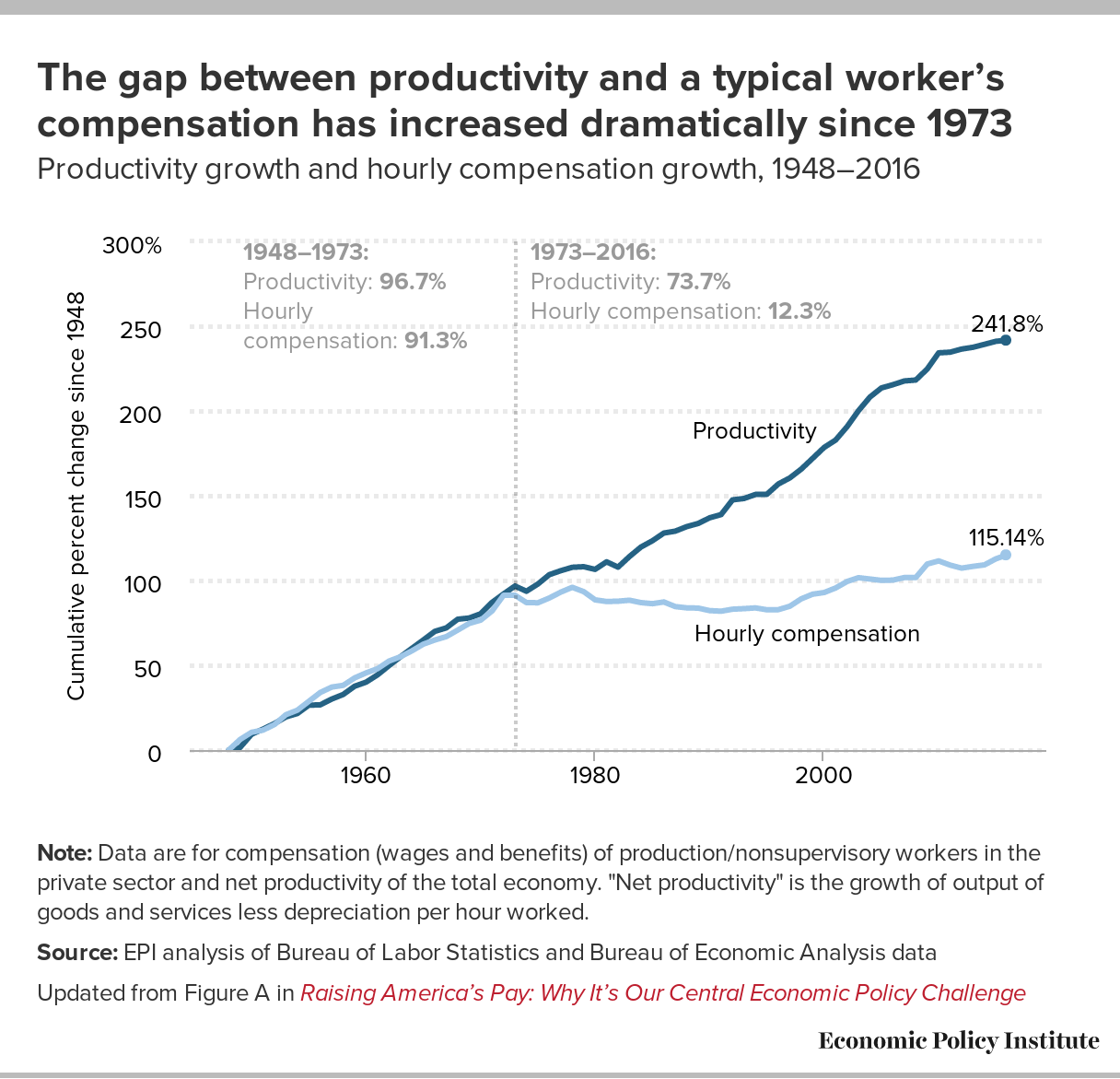

I work at the Economic Policy Institute, a think tank that has devoted enormous effort to understanding trends in American pay. For years our flagship publication has been the State of Working America, and in 2014, we launched the Raising America’s Pay initiative. We were the first to notice the divergence between economywide productivity and hourly pay for typical workers, and we have been the loudest voice inside the Beltway demanding that policymakers address the crisis in American pay.

These years of studying labor market outcomes led us to realize that policy decisions that affect workers’ leverage and bargaining power vis-à-vis their employers are enormously important in determining whether paychecks grow. Put simply, if a worker can’t credibly threaten to impose real costs on their employer if bargaining over wages breaks down, they have very little chance of getting raises. This explains why collective bargaining is so central to achieving healthy wage growth: If bargaining breaks down between an employer and a single worker, that doesn’t disrupt business too much. If the bargaining breakdown leads to an entire workforce not showing up to work, it’s a different story.

Similarly, if a worker threatens to leave a job unless they get a raise when the overall unemployment rate is very high, both sides know that the employer will be able to replace them easily with somebody currently jobless, so the threat isn’t credible. But if a worker threatens to leave when overall unemployment is low, the employer will have a much harder time recruiting to replace them, and the threat is real. This explains why wages grow faster when the economy booms and labor markets are tight.

Republican policymakers and their advisers are not likely to embrace this diagnosis of why wages have not grown anytime soon, but they do now realize the basic facts about sluggish growth in pay and its political salience. “We want our companies to hire & grow in AMERICA, to raise wages for AMERICAN workers, & to help rebuild our AMERICAN cities and towns!” President Trump declared in September. He and his GOP allies know they need to offer something they can claim is a wage-boosting policy, and they’ve decided that tax cuts will be this something.

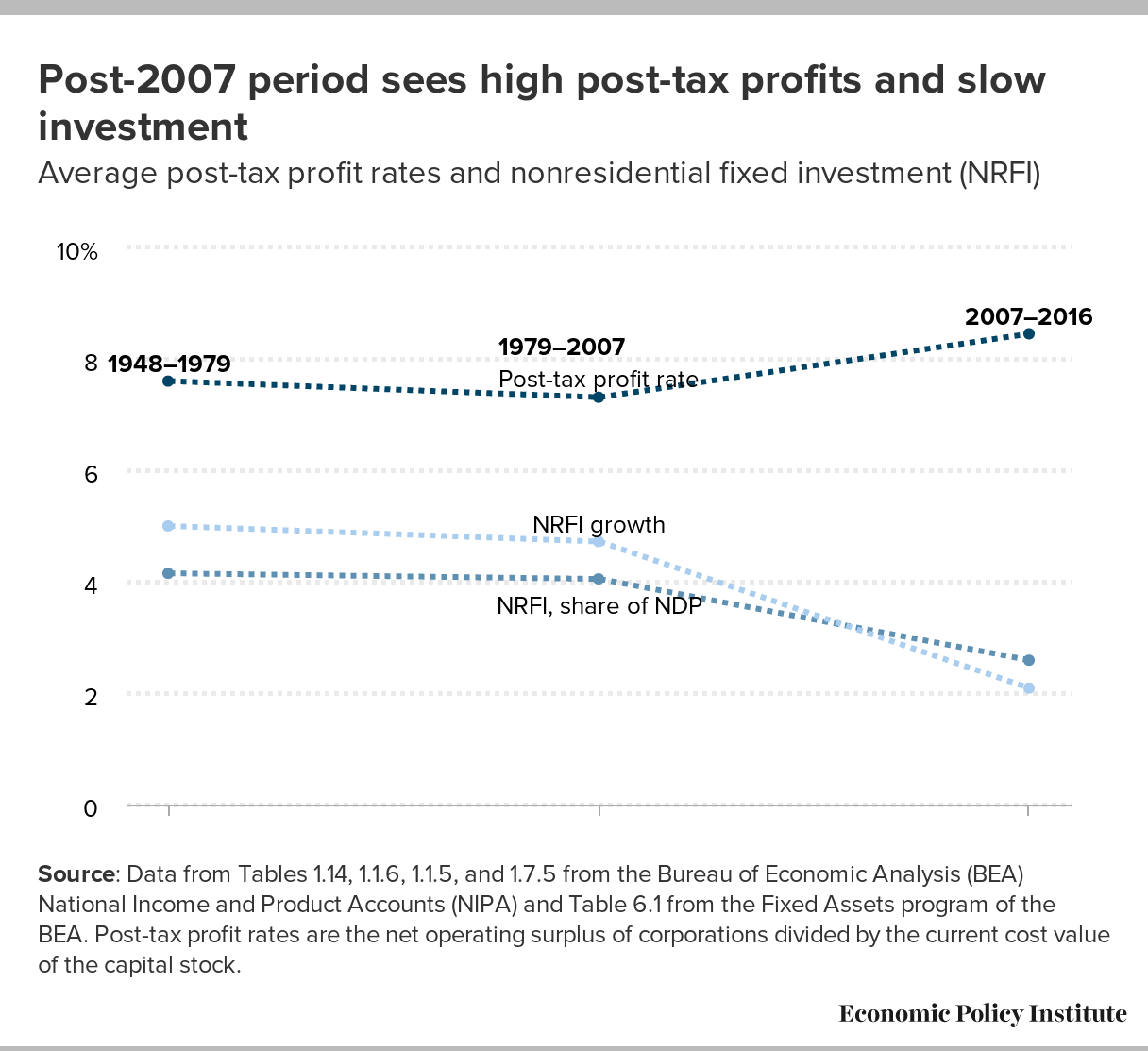

It’s true that the economics textbook does offer them some support here. If post-tax profit rates were low and the cost of obtaining capital (or interest rates) were high, then corporate rate cuts (that were fully paid for) could in theory spark a chain-reaction of events that lead to higher wages. A corporate rate cut would boost post-tax profitability, which could spur firms’ demand for making productivity-enhancing investments. The savings needed to finance these investments could come from households saving more in response to the higher returns to corporate stock ownership. The resulting increased investment in plant and equipment would boost workers’ productivity, and this boost to productivity would make wage gains possible.

Why isn’t this series of bank-shots likely to work in the real world?

First, post-tax profitability has been historically high for years now while interest rates have been low. Yet business investment has been extraordinarily slow. Clearly, something besides depressed profitability or high interest rates is holding investment back. Second, real-world evidence — from the historical experience of the U.S. economy after tax cuts to international comparisons to the experience of U.S. states that have cut business taxes — offers no serious reason to think a wage bonanza will follow these tax cuts. Third, if corporate rate cuts are not paid for with spending cuts or other tax increases, then the boost to private savings they provide will be neutralized by a reduction in public savings (i.e., a rise in the federal budget deficit). This will choke off the financing needed to boost investment in productivity-enhancing plant and equipment by raising interest rates. Finally, without measures to boost workers’ leverage and bargaining power, there is no guarantee that any gains to productivity would actually reach employees’ paychecks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

In the end, a strategy of increasing workers’ leverage and bargaining power has a much higher likelihood of success in boosting wages. Ironically, corporate tax cuts aren’t just useless as a wage-booster, they’re likely even worse at spurring business investment than measures to boost typical workers’ leverage and bargaining power. Why? Because if wages finally do start rising reliably, that could lead firms to worry about higher salaries eating into profit margins and start to make productivity-enhancing investments to cut labor costs.

See: McKinsey Global Institute (MGI), Jobs Lost, Jobs Gained: Workforce Transitions in a Time of Automation (December 2017) (Scribd). The economy of most countries will eventually replace the jobs lost, the study says, but many of the unemployed will need considerable help to shift to new work, and salaries could continue to flatline.

We’re happy to welcome Republicans’ newfound recognition that American workers need a raise. But we’ll hold our applause until they offer real solutions. Tax cuts for America’s richest businesses does not count.

Well said.

Discover more from Blog for Arizona

Subscribe to get the latest posts sent to your email.

Shows how the strong the Obama economy keeps chugging along. At least until the Repugs get their beloved tax cuts and the cuts have their effect. At which point Deadbeat Donnie will cease taking credit and start blaming Obama.

A few months ago there was a picture going around of Barrack and Michelle Obama standing next to Donald and Melania Trump at Trump’s inauguration with the caption:

“Dear Racists, the White Man in this picture is the one with five different children from three different women.”

Too bad for crass and boorish Donald Trump, his money can’t buy him Obama’s class and intelligence.

Trumpaloompa’s will never acknowledge the previous 8 years of job growth and stock market gains. Because of all the black.

I remember seeing that. A shame the message will never sink in with his hardcore evangelical dead-enders.

“At least until the Repugs get their beloved tax cuts and the cuts have their effect.”

And the sky will begin to fall, great cracks will appear in the earth, the four horse men of the Apocalypse will be seen, and the smell of fire and brimstone will saturate the air.

Under Obama, things did get better. Your hope that the economy under Trump will collapse seems sort of desperate and silly in light of reality.

Steve! Long time no see! Was beginning to think that bridge you live under collapsed due to lack of infrastructure maintenance!

Where do you get this nonsense that liberals/progressives want your Dear Leader to fail? As I recall, as the Secret Kenyan Muslim was first being inaugurated your heroes such as the Vulgar Pigboy Limbaugh was loudly proclaiming “I hope he fails” and Miss McConnell vowing along with his fellow Repugs to ensure that the Secret Kenyan Muslim was a one term president. And you probably happily went along with it.

I’ve said it before and I’ll say it again. You really need to get your head out of the right wing media sewer before the brain damage is permanent.

“Steve! Long time no see! Was beginning to think that bridge you live under collapsed due to lack of infrastructure maintenance!”

Thanks for noticing I was missing! I took some of the family and went to China for a few weeks. What an amazing history that place has! So much to see! But it is good to get back home.

“Where do you get this nonsense that liberals/progressives want your Dear Leader to fail? “

Some things, Willeybud, are intuitively obvious to even the most casual observer. The democrats and their cronies have done anything they can do to keep Trump from accomplishing anything. Even the one time Trump worked with the democrat leadership, he was vilified, cursed and thwarted in what he was trying to do. You really have to hate someone to keep condemning him when he is trying to agree with you. It just shows that there is no actual agenda for the leftexcept the destruction of Trump. You are slipping into that liberal double-speak where you deny you are doing something even if we are watching you do it.

It is a little like that old story about the democrat Senator whose wife caught him in bed with another women. Before she could say anything he hollered out: “Are you going to believe me or your lying eyes”.

Anyway, it is good to hear from you, Wileybud…

1. It’s not an old story, it’s a Richard Pryor routine, no Democrats were involved.

2. If your Dear Leader is vilified & cursed it’s because he’s an irredeemable scumbag. True, he did work with Pelosi & Schumer on one thing but a scumbag is still a scumbag. Guess you’re also a fan of Admiral Darlan?

3. I posted this three days ago, took you that long to come up with something?

4. We on the left have quite the agenda – lessening income inequality, lessening sexual equality, a fairer political system that’s not ruled by those with most of the gold, equal justice for all (including holding the wealthy accountable for their actions), etc. Of course that’s hard to see when you’re obsessed with inaccurately cliched stereotypes of those with whom you disagree.

“Sounds so democratic”… there’s your right wing nut thinking right there.

It just “sounds” true.

LOL.

This response to Wileybud is out of sequence because there were no “reply” options available.

“It’s not an old story, it’s a Richard Pryor routine, no Democrats were involved.”

Actually, it is a Marx Brothers routine from the 1933 movie “Duck Soup”. But it just sounds so “democrat”…

“Guess you’re also a fan of Admiral Darlan?”

No, I am rather indifferent to him. What I can’t figure out is why you think there is a relevancy to this subject.

“I posted this three days ago, took you that long to come up with something?”

Don’t flatter yourself…I only saw it a few minutes before I posted my response. I enjoy posting here, but it is a relatively low priority for my time.

“Of course that’s hard to see when you’re obsessed with inaccurately cliched stereotypes of those with whom you disagree.”

Do you know why stereotypes exist? It is because there is always a measure of truth in them. In the case of democrats, the stereotype developed over a period of almost 200 years. The essence of the party has not changed much since it’s founding in 1830. Big government, heavy taxation, the curtailment of individual liberties for the sake of the group, the indenturement of citizens to the government for handouts…this is the democrat party and it always has been.

What part of “inaccurately” do you not understand?

And finally, besides yourself who do you think you’re kidding?

During the dotcom bubble I worked in Silicon Valley, and we all knew it was a bubble, in spite of the “Cheerleaders of the Apocalypse” on CNBC.

We just didn’t know what was going to make it go “pop”.

We sold a house in California to move to AZ and made a ton of money on the Cali house.

Then we watched the base model of our AZ home, under construction, go up 80 grand in six months. Before we ever moved in.

And because I knew we were in a bubble, I kept hoping that was enough to buffer us when the obvious housing bubble burst.

It was not. Worst haircut ever. Thanks Bush!

We knew it was a bubble but didn’t know what would make it go “pop”.

The next few years is going to be interesting. Who is holding the bubble popping pin?

I’d bet it’s going to be the massive corporate and billionaire tax cuts, and massive deregulation, leading to some very irrational behavior by the same people who should be in prison after they caused the Bush Recession.

But I base that on history, so unless history starts repeating itself….

Oh, shit!