By Craig McDermott, crossposted from Random Musings

…And, apparently, Arizona’s legislators don’t think that Arizona’s voters were thorough, or clear, enough in 2008 when we soundly rejected their payday loan legalization proposal in that year’s election.

Payday loans were short term cash loans with usurious interest rates (400%!). The loophole in Arizona law that exempted them from the 36% cap for an annual interest rate expired in 2010, and while there have been periodic efforts by legislators to revive them, those have all failed.

Well, Arizona’s legislators are nothing if not persistent.

On Monday, the House Ways and Means Committee will hear a striker to SB1316.

If enacted, it would bring back payday loans by another name, “flexible credit loans”. Such “loans” would carry an annual interest rate of “only” 204%.

The bill is being pimped pushed by an astroturf (fake grassroots, but it doesn’t look like that they are putting much effort into hiding who is behind this) group named “Arizona Financial Choice Association’ (AFCA) –

|

| From my FB feed, 2/27/2016 |

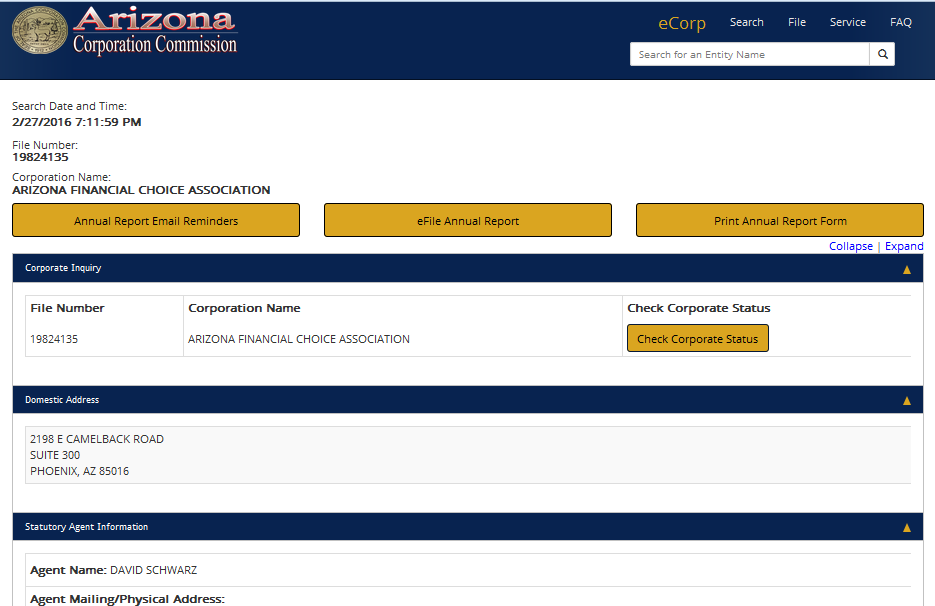

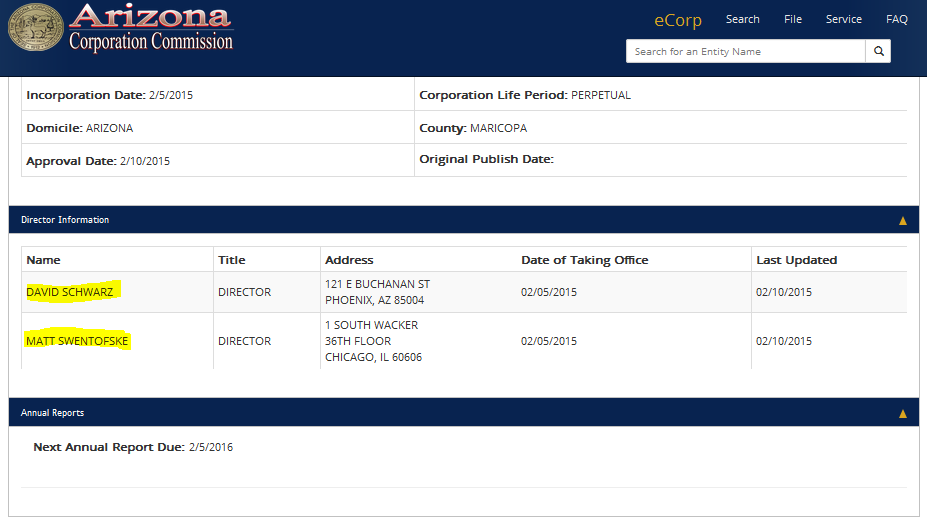

A quick check of records at the Arizona Corporation Commission turns up this –

A little quick research into the two listed “directors” turned up strong ties to the legal loansharking industry –

In other words, the FB ad pushed by this group is partially correct – people *should* contact their legislators about this bill.

And let them know that we are watching.

Discover more from Blog for Arizona

Subscribe to get the latest posts sent to your email.

Interesting information – thanks. Would you go further into the interest rate issue. All the press releases on this bill do not mention interest rates, and an examination of the bill’s language, specifically Section 6-1832, indicates finance charge rates are 1) 17 percent per month if unsecured, 2) 15% if secured with personal property, and 3) may not be compounded. Prohibited Acts, Section 6-1811, declare annual rates for certain protected people, active armed forces personnel among others, are restricted per federal law. It looks like 36%. On the other hand, Arizona Usury Law, specifically A.R.S. 44-1201 states the interest on any loan shall be at a rate no more than 10% unless the rate is written down. This is a confusing issue. How did you come up with 204%, and how does that square with language of the bill and with the usury law?