As insurers exit “ObamaCare” marketplaces across the country, critics of the Affordable Care Act have redoubled their claims that the health law isn’t working.

Not surprisingly, many of these critics are Tea-Publican politicians in red states who actively took steps over the last several years to sabotage the 2010 law and fuel the current turmoil in their insurance markets. The states with the biggest Obamacare struggles spent years undermining the law:

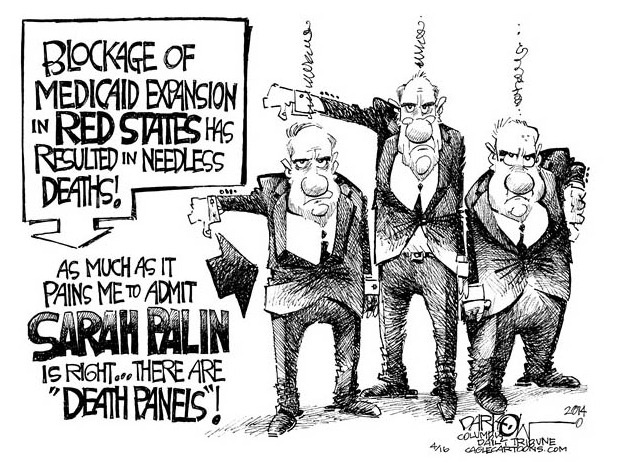

Among other things, they blocked expansion of Medicaid coverage for the poor, erected barriers to enrollment and refused to move health plans into the Obamacare marketplaces, a key step to bringing in healthier consumers.

Among other things, they blocked expansion of Medicaid coverage for the poor, erected barriers to enrollment and refused to move health plans into the Obamacare marketplaces, a key step to bringing in healthier consumers.

Those decisions left the marketplaces in many red states with poorer, sicker customers than they otherwise might have had.

Now, consumers are paying the price, as insurers seek major rate hikes or stop selling plans altogether.

This is not a failure of “ObamaCare” — it is a failure of red state Tea-Publican politicians who actively sabotaged the health care law rather than experiment with state-run insurance marketplaces to make health insurance more efficient and affordable, as the law provided.

Eight of the nine states where consumer choices will be most limited in 2017 have rejected Medicaid expansion and taken other steps that have weakened their marketplaces, data show.

“It’s the same basic lesson I tell my kids,” said Manatt Health managing director Joel Ario, a former insurance commissioner in Oregon and Pennsylvania. “If you put the work into something, you will get results. If you just sit on the sidelines and complain, you shouldn’t be surprised if things don’t work out.”

The marketplaces have been shaken by the closure of more than a dozen new insurance co-ops and moves by major national insurers, including UnitedHealth Group, Humana and Aetna, to scale back offerings in 2017. Many of the insurers that remain in the marketplaces are seeking double-digit rate hikes.

Nearly all cited unsustainable losses due to sicker, and thus costlier, customers than the health plans anticipated.

The market exits have left consumers in wide swaths of the country with diminishing choices going into 2017.

In nearly a third of counties nationwide, just a single insurer will offer plans next year, according to an analysis by the nonprofit Kaiser Family Foundation.

That has fueled a new round of criticism from Republican politicians.

* * *

The marketplaces, which currently provide coverage to about 11 million Americans, were supposed to be more competitive.

The law’s architects hoped insurers would be drawn in by the opportunity to sell health plans to millions of Americans. They also included provisions in the law to bring in healthy customers most prized by insurers, included federal subsidies, which help defray most consumers’ monthly premiums. Americans who don’t have coverage are subject to tax penalties.

Importantly, the law also depended on states to support their marketplaces and help enroll healthy consumers.

The ACA designated the state’s governor as the decision maker for establishing a state-run insurance marketplace. If the state did not set up an insurance marketplace, the default was the federal marketplace. Governor Jan Brewer refused to establish a state-run insurance marketplace, forcing Arizona into the the federal marketplace by default. Arizona does not actively support enrollment in the federal marketplace.

Like all insurance, the Obamacare marketplaces require a mix of policyholders, or “risk pool,” so lower-cost participants offset the higher medical costs of sicker customers.

State insurance regulators were to phase out health plans that insurers had been offering before 2014, thereby moving those policyholders into the marketplaces. These customers were overwhelmingly healthy because prior to 2014 insurers in most states largely didn’t sell plans to people with preexisting medical conditions.

States were also offered millions of dollars in federal aid for outreach and enrollment efforts starting in 2013.

Marketing was seen as critical since sick customers were expected come to the marketplaces on their own, while younger, healthier consumers would probably need to be educated about the importance of getting coverage.

“The assumption was that states would play an active role,” said Jon Kingsdale, who ran the Massachusetts marketplace that became the model for the federal law.

Some states, including California, Connecticut and Maryland, did.

State officials there and elsewhere also worked closely with insurance companies to get them into the markets so consumers would have more choices. California spent hundreds of millions of dollars on outreach campaigns.

“States like California that made tough decisions early on and used all the tools available have competitive markets, with opportunities for consumers to choose plans,” said Peter Lee, head of Covered California, the state’s marketplace.

California and other states that actively supported the law haven’t been immune to the current market turmoil, as many factors have affected their marketplaces and helped drive up premiums for 2017.

But even with some market exits, consumers in more than half of California counties can choose from at least three insurers when selecting health plans next year. That means many will probably be able to find lower-priced options even though some insurers are planning double-digit rate hikes for 2017.

There are many fewer options in states whose leaders have spent years working to sabotage the law.[Like here in Arizona.]

There are many fewer options in states whose leaders have spent years working to sabotage the law.[Like here in Arizona.]

These include Alabama, Alaska, Florida, Mississippi, Missouri, North Carolina, Oklahoma and Tennessee, all of which will have only one insurer in most counties next year, according to the Kaiser analysis.

Building viable insurance marketplaces in some of these states always figured to be challenging, as competition was limited before the law was enacted.

But many of these states made it even more difficult.

Several are among the more than a dozen that imposed additional regulations on people who were supposed to help consumers enroll in health plans.

Proponents of these regulations argued they were trying to protect consumers. “Our biggest fear, of course, is identity theft,” Florida Atty. Gen. Pam Bondi told Fox News in 2013.

But consumer advocates, patients groups and others saw the rules as another tactic to weaken the law. Missouri’s regulations were so restrictive that they were thrown out by a federal judge, who concluded state leaders were trying to undermine the marketplace.

Insurance regulators in more than three dozen states, facing a backlash from consumers, also refused to move customers with health plans that predated the health law into the marketplaces.

And 19 states are still rejecting federal aid to expand their Medicaid programs to poor, childless adults, a group of Americans traditionally excluded from the government safety net.

36 of Arizona’s Tea-Publican state legislators filed a lawsuit in 2013 challenging HB 2010, the expansion of Medicaid bill, signed into law by Governor Jan Brewer. The Superior Court for Maricopa County ruled against them in August 2015. Opinion (.pdf). The case is still an active appeal to the Court of Appeals (1 CA-CV 15-0743). No final decision has been entered.

This has been particularly problematic for those states’ marketplaces, research suggests, as many poor – and probably sick – residents who couldn’t get Medicaid have gone into the marketplaces.

Federal data indicate that more than 40% of marketplace enrollees in states that didn’t expand Medicaid earn less than 138% of the federal poverty level, or about $16,000 a year.

By contrast, less than 10% of marketplace enrollees in states that expanded Medicaid are so poor.

Americans making less than 138% of the federal poverty level qualify for Medicaid coverage in expansion states.

Obama administration officials are now working to adjust marketplace rules for 2018 in an effort to bring in more younger, healthier customers.

And last week, Health and Human Services Secretary Sylvia Burwell sounded an upbeat note, explaining that the new rules should make the marketplaces more attractive for insurers in the future.

It remains to be seen whether more states will help, however.

There will not be any help from Arizona’s Tea-Publican congressional delegation or state legislators. If you need “ObamaCare” insurance or Medicaid (AHCCCS) for health insurance, your only option is to vote these Tea-Publcan politicians out of office and begin to reverse the effects of their active sabotage of “ObamaCare.”

Your alternative is the GOP healthcare plan: “perhaps you should die and decrease the surplus population.”

Discover more from Blog for Arizona

Subscribe to get the latest posts sent to your email.

There are other matters that are starved by State government and then the claim is made they are not working. Remember anytime Ducey and the legislative majority say the work “reform” you can guarantee a disaster is in the making.

1. Education funding. 48th or 49th among the 50 states. “Reform” means give more tax money to private charters or private religious schools.

2. Southern Arizona Mental Health funding. We need more “efficiencies”. Funny how the mentally ill and drug addicts don’t naturally respond to service “efficiencies”. So it makes sense to the pinheads to have it administered by a FOR PROFIT agency, on a subrecepient, reimbursement basis. So they make reimbursements incredibly difficult, and make up numerous reasons why they won’t reimburse after the service is delivered. How else can you make a profit?

3. Watch out there is a national effort, led by ALEC, for State level “regulatory reform” to remove”barriers” from independent boards who regulate professions. This national effort is designed to consolidate the regulation of these professions in Republican governors offices. They can then do for professions what they have done for voting rights. The first assault was on, of all things, athletic trainers. After all any untrained aide can do a concussion protocol. This one wasn’t dropped last session until the Suns, Cardinals, Diamondbacks, Wildcats, and Sun Devils professionally licensed trainers got involved. But look out, they will cite nail technicians and cosmetologists, but will be after geologists, surveyors, architects, engineers, and the health professions, after all any knucklehead can do those jobs.

you just found out? I would ask YOU what YOU are going to do about besides whine :but I already know the answer NOTHING!