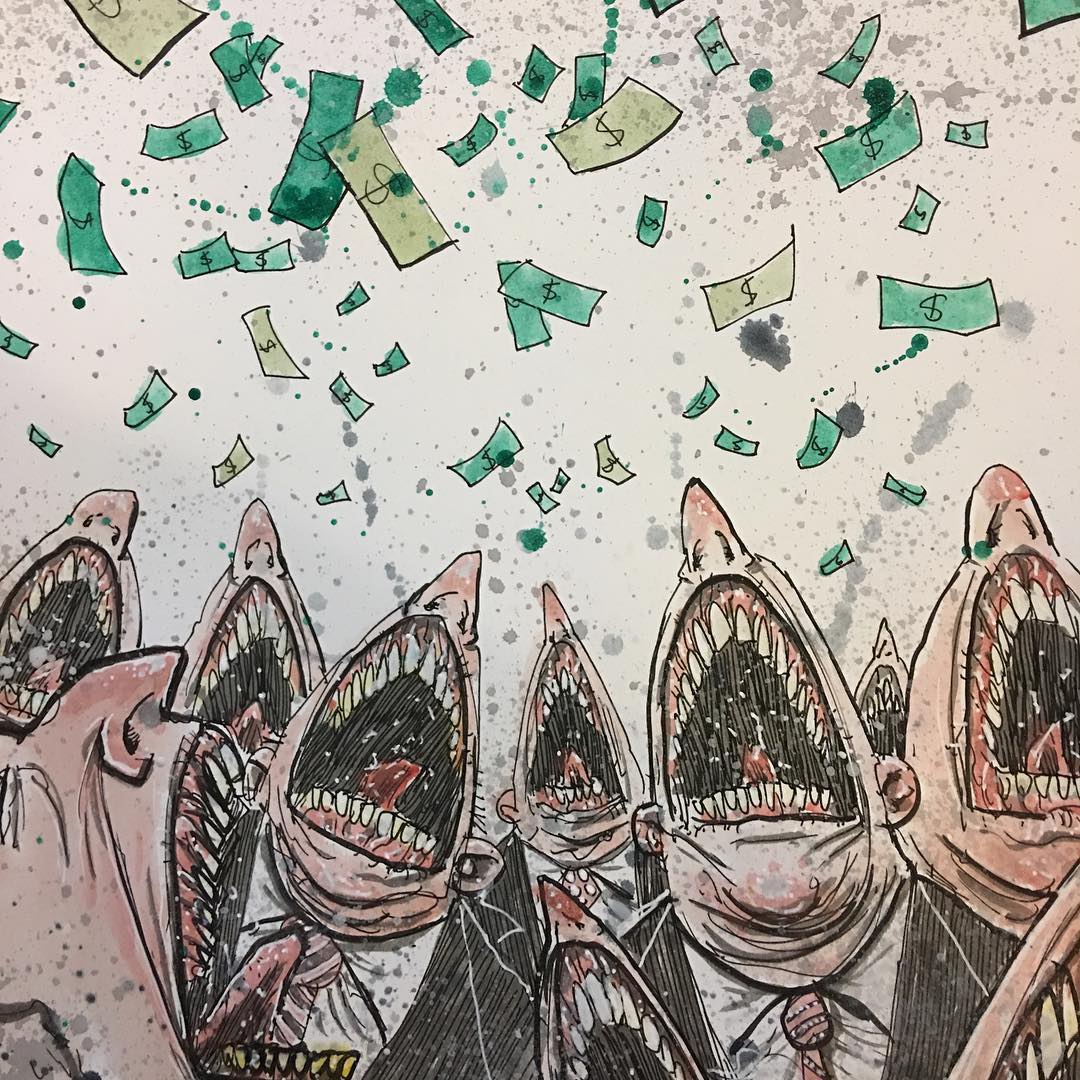

Only a decade after the banksters of Wall Street engaged in casino capitalism and the largest fraud ever perpetrated in human history, nearly destroying the world’s financial system and causing the Great Recession, the banksters of Wall Street have reasserted their stranglehold over members of the U.S. Congress.

Only a decade after the banksters of Wall Street engaged in casino capitalism and the largest fraud ever perpetrated in human history, nearly destroying the world’s financial system and causing the Great Recession, the banksters of Wall Street have reasserted their stranglehold over members of the U.S. Congress.

In a 67-31 vote, the U.S. Senate approved the most sweeping changes yet to Dodd-Frank that have earned bipartisan support. All present Republicans and 16 Democrats and Independent Angus King voted to approve the measure, sending it to the House.

Bennet (D-CO), Carper (D-DE), Coons (D-DE), Donnelly (D-IN), Hassan (D-NH), Heitkamp (D-ND), Jones (D-AL), Kaine (D-VA), Manchin (D-WV), McCaskill (D-MO), Nelson (D-FL), Peters (D-MI), Shaheen (D-NH), Stabenow (D-MI), Tester (D-MT), Warner (D-VA); King (I-ME).

The Washington Post reports, Senate passes rollback of banking rules enacted after financial crisis:

The Senate on Wednesday passed the biggest loosening of financial regulations since the economic crisis a decade ago, delivering wide bipartisan support for weakening banking rules despite bitter divisions among Democrats.

The bill, which passed 67 votes to 31, would free more than two dozen banks from the toughest regulatory scrutiny put in place after the 2008 global financial crisis. Despite President Trump’s promise to do a “big number” on the Dodd-Frank Act of 2010, the new measure leaves key aspects of the earlier law in place. Nonetheless, it amounts to a significant rollback of banking rules aimed at protecting taxpayers from another financial crisis and future bailouts.

Given the bipartisan support for the bill, Wednesday’s passage was expected. But for the first time since Trump became president, the divisions lurking within the Senate Democratic Caucus burst into full view, with Sens. Elizabeth Warren (Mass.) and Sherrod Brown (Ohio) leading vehement opposition to the bill, even as supporters — including Democrats up for reelection in states Trump won — supported it with equal vigor.

Warren and Brown argued the bill amounts to a gift to Wall Street that increases taxpayer risk while boosting the chances of another financial crisis. Supporters of the legislation — including endangered Democratic Sens. Heidi Heitkamp (N.D.), Joe Donnelly (Ind.) and Jon Tester (Mont.) — disputed that characterization, contending that the bill’s aim is to loosen onerous regulations on local banks and credit unions, freeing them to focus more on community lending, particularly in rural states.

“It is a bill that I am incredibly proud of,” Heitkamp said in a Senate floor debate this week. “Dodd-Frank was supposed to have stopped too big to fail, but the net result has been too small to succeed. The big banks have gotten bigger since the passage of Dodd-Frank, and the small banks have disappeared.”

Following Heitkamp on the floor, Warren condemned the legislation as “the bank lobbyist act” and said it “puts American families in danger of getting punched in the gut.”

“Washington is poised to make the same mistake it has made many times before, deregulating giant banks while the economy is cruising, only to set the stage for another financial crisis,” Warren said.

Senate Minority Leader Charles E. Schumer (D-N.Y.) opposed the legislation but has played little role in a debate that has allowed liberals and moderates in his caucus to stake out positions tailored to their own political needs. But after Warren called out red-state Democrats and other supporters of the bill by name in a fundraising appeal, Schumer encouraged her to stay focused on the substance in the debate, according to a person familiar with the exchange who requested anonymity to discuss it.

Few of the Democrats named by Warren wanted to comment publicly on dissension within the caucus. Heitkamp downplayed their disagreements, saying of Warren in an interview, “She feels very, very strongly about this. I think it’s a difference between where we’ve always been on these banking issues. And you know obviously as you’re moving the bill forward, these differences were going to come to a head, and we were going to see a conflict because I just don’t see the bill the way she does.”

It’s not clear whether the Democratic divisions laid bare by the banking bill will resurface anytime soon, given the light legislative schedule expected in the Senate for the remainder of this midterm election year. But the debate highlighted how the political imperatives for red-state Democrats can collide with those of liberals such as Warren, who’s seen as a potential presidential candidate in 2020, creating the potential for conflict that could flare anew in future.

Banks with more than $50 billion in assets are now considered “too big to fail” and are subject to the toughest regulations, including a yearly stress test to prove they could survive another period of economic turmoil. The Senate legislation, shepherded by Banking Committee Chairman Mike Crapo (R-Idaho), would raise that threshold to $250 billion in assets, potentially allowing several high-profile financial institutions, including American Express, Ally Financial and Barclays, to escape the extra regulatory scrutiny.

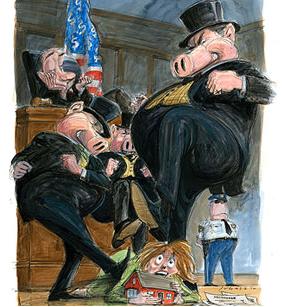

The bill’s supporters say these banks have been unfairly saddled with regulations originally intended for global behemoth banks such as JPMorgan Chase, not regional or midsized firms. Lifting the restrictions would save the industry billions a year in compliance costs, industry analysts say. It would also make it easier for them to reward shareholders with dividends and stock buybacks, they say [i.e., the The Predator Class one precent must be appeased.]

The bill’s supporters say these banks have been unfairly saddled with regulations originally intended for global behemoth banks such as JPMorgan Chase, not regional or midsized firms. Lifting the restrictions would save the industry billions a year in compliance costs, industry analysts say. It would also make it easier for them to reward shareholders with dividends and stock buybacks, they say [i.e., the The Predator Class one precent must be appeased.]

Democrats and advocacy groups warn that the push to loosen the regulations fails to recognize that many of the midsized institutions that would be helped by the Senate legislation fell into dire financial straits less than a decade ago and needed more than $40 billion in taxpayer bailouts. During a financial crisis, they say, banks tend to fail in tandem, suffering from similar ailments. And the failure of several in a short time period could strain the U.S. economy.

The bill has largely been marketed as long-overdue help for small community banks and credit unions. The legislation, for example, would exempt banks with less than $10 billion in assets from the “Volcker rule,” which bars banks from making risky wagers with their own money [casino capitalism]. The bill would also exempt many small banks from a Dodd-Frank requirement that financial institutions report more detailed data on whom they lend to. The industry has complained that both measures are too cumbersome and time-consuming.

Exempting small banks from the mortgage data requirement would weaken the government’s ability to enforce fair-lending requirements, making it easier for community banks to hide discrimination against minority mortgage applicants and harder for regulators to root out predatory lenders, consumer advocates say. The Senate rolls back rules meant to root out discrimination by mortgage lenders:

Exempting small banks from the mortgage data requirement would weaken the government’s ability to enforce fair-lending requirements, making it easier for community banks to hide discrimination against minority mortgage applicants and harder for regulators to root out predatory lenders, consumer advocates say. The Senate rolls back rules meant to root out discrimination by mortgage lenders:

The provision “would exempt 85 percent of banks and credit unions from the new requirement, according to a Consumer Financial Protection Bureau analysis of 2013 data.”

Congress had charged the Consumer Financial Protection Bureau, an independent watchdog agency formed after the financial crisis, with collecting, analyzing and publishing the data. But White House budget director Mick Mulvaney, named the CFPB’s acting director last November, said the agency plans to reconsider the new requirements, and that banks would not be penalized for data collection errors in 2018. He also stripped the bureau’s fair-lending office of its enforcement powers.

The Senate bill repeals many of the new reporting requirements, exempting small lenders making 500 or fewer mortgages a year from the expanded data disclosure.

“Banks say they don’t treat borrowers differently, but the data shows a different story,” said Sen. Catherine Cortez Masto (D-Nev.) on the Senate floor last Thursday. “Redlining remains a major problem for communities of color.”

A February report by the Center for Investigative Reporting showed that redlining persists in 61 metro areas — from Detroit and Philadelphia to Little Rock and Tacoma, Wash. — even when controlling for applicants’ income, loan amount and neighborhood, according to its analysis of Home Mortgage Disclosure Act records.“

By stripping away important regulations to hold banks accountable, we are risking another financial crisis that is rooted in unfair lending practices,” Cortez Masto said in a statement Wednesday night.

The bill still needs to be approved in the House, where Republicans have been pushing a more aggressive rollback of financial regulations. That chamber passed a bill last year that stripped the Consumer Financial Protection Bureau, created under Dodd-Frank, of much of its power, for example. But the future of the CFPB is not addressed in the Senate bill.

Rep. Jeb Hensarling (R-Texas), chairman of the House Financial Services Committee, has said that House Republicans will want to alter the Senate bill to reflect their priorities. But that could drive away the Senate Democrats needed to pass the legislation [really? All 16 of them?], and so the House will face significant pressure to accept the Senate legislation with few, if any, changes.

Although the banking bill marked the first bipartisan legislation of the Trump era aside from must-pass spending deals, it was far from a freewheeling debate on the floor. Because of disagreement between the parties that has become routine, no amendment votes were permitted, frustrating senators in both parties who hoped to advance favored policies.

Sen. Bob Corker (R-Tenn.), a member of the Banking Committee, had been pushing an amendment to strike a section of the bill that could reduce the capital cushions of five of America’s biggest banks. Though supported by liberal Senate Democrats, it never came up for a vote amid the wrangling over the amendment process.

The Hill adds, Senate passes bipartisan bill to roll back Dodd-Frank:

On Wednesday, senators voted by the same tally to end debate on the legislation and approve a set of changes to the bill, with many aimed at warding off liberal criticisms of the measure.

The amended measure clarifies that foreign banks with U.S. holdings less than $250 billion but above that level in foreign assets would still be subject to closer oversight. Provisions to force credit bureaus to offer free services for victims of hacks, protect military veterans from fraud, create new student loan backstops and mandate studies on various risks to the financial system were also added to the bill.

Senators filed more than 100 other amendments to the bill, but party leaders did not reach a deal to bring any of them up for a vote. Sponsors of the bill have resisted major changes over fears they could ruin the delicate bipartisan deal.

The bill’s future in the House is uncertain. The measure is seen by critics of Dodd-Frank as perhaps the last, best chance of a major legislative revision to the 2010 rules. Republicans are also eager to tout a major rollback of Obama-era rules as they head into the midterm elections.

But the Senate bill makes far fewer and weaker changes to Dodd-Frank than those sought by the House. Conservatives that spearheaded the House’s 2017 bill to rewrite Dodd-Frank want to add several measures intended to take a bigger chunk out of the law.

Rep. Jeb Hensarling (R-Texas), chairman of the House Financial Services Committee, said Tuesday he’s not holding talks with key senators on making changes to the bill. He’s called on the Senate to add to their package a list of more than two dozen financial deregulation bills passed by his panel with bipartisan support.

Other House Republicans say they want to pursue changes with the Senate and form a conference committee to strike a deal, but seemed more open to the bipartisan bill.

K Street sources told The Hill that the measure faces growing opposition in the House, but Senate Democrats backing the bill have opposed reopening the bill after sending it to the lower chamber.

“There are some out there who say ‘this bill is going to look completely different when it comes back from the House.’ It may. If it does, than I guess we’re done,” Sen. Jon Tester (D-Mont.) said last week.

So this fight is not yet over. Maybe it’s time to bring back a renewed Occupy Wall Street movement. Protest movements are all the rage these days.

Discover more from Blog for Arizona

Subscribe to get the latest posts sent to your email.

For a contrarian view, see Michael Grunwald at POLITICO, Behind the Dodd-Frank Freakout https://www.politico.com/magazine/story/2018/03/17/behind-the-dodd-frank-freakout-217645?lo=ap_f1

“There are plenty of legitimate questions about why Congress feels the need to provide regulatory relief to banks that are already enjoying record profits, and whether some of the bill’s tweaks to Dodd-Frank will make the financial system less safe. But the doomsday rhetoric about those tweaks—and the political rift they are creating within the Democratic Party—seem extreme compared to their substance. The Senate bill leaves the vast majority of the Dodd-Frank reforms in place, which is why House Republicans who hate Dodd-Frank are already signaling they won’t allow it to become law. The critiques of the bill as a giveaway to Wall Street megabanks seem particularly overblown: Very few of its changes would affect the dozen or so institutions that pose the largest potential dangers to the financial system.”

If I heard correctly Barnie Frank supports the bill. Is that correct? If so I’m inclined to think it isn’t as bad as Warren and Brown would have us believe.

You heard wrong. Barney Frank wrote this op-ed for CNBC, “Why I would vote ‘no’ on Senate bill to amend Dodd-Frank” https://www.cnbc.com/2018/03/01/barney-frank-why-i-would-vote-no-on-senate-bill-to-amend-dodd-frank-commentary.html

“While I share the view of many of the pro-reform Senate Democrats who have accepted this package that responding to the concerns of small and midsized banks has both substantive and political arguments in its favor, I believe that the price the Republican colleagues are demanding is too high.

* * *

If I were still a member of Congress, I would vote no on this package without amendments fully restoring the law regarding housing discrimination, reducing the FSOC level to $125 billion, and eliminating both the restrictions on the FSOC’s power to reach down and the specials rules for foreign mega-banks.

I understand why the Democrats who support the package believe that its positive elements outweigh these negatives, and I agree that one of the most important positives is that passing the Senate package into law is in effect a ratification of all the other parts of the law. But I disagree based in part on what is in the bill, and by two factors outside the parameters of the amendments.

One is the ability of President Trump’s appointees to employ the parts of the amendments I find problematic in the way most damaging to reform. The other is the stated intention of the House Committee leaders to press the Senate into accepting some of their anti-reform proposals. I am encouraged that the Democrats who sponsor the amendments have said that they will resist such effort, but I understand why this makes many of the most pro-reform elements nervous.

While I do agree with those with whom I have been allied in this effort that the bill should not pass as written, some disagreements remain.

* * *

I most strongly disagree with advocates who in this case as in others treat a fairly narrow dispute over one issue as if it were a betrayal of basic principles. If Senators from states that voted for Donald Trump who have voted against his tax cut, for the preservation of the Affordable Care Act, and in this case for protection of most of the Dodd-Frank Act are treated as enemies, we progressives too few friends to be effective.”

Thanks for the clarification!